Podcasts

Watch videos featuring supply chain experts

The world has not stopped trading. It has simply found new roads. Since 2022, a record volume of economic sanctions has been deployed against Russia, Iran, Myanmar, and a growing list of entities worldwide. Russia has become the world's most sanctioned economy, yet its exports to China and India have expanded significantly even as trade with Western markets collapsed. Governments imposed them expecting trade to shrink. Instead, trade adapted a route which are quiet, efficient, and often invisible to the untrained eye.

The problem is not that sanctions fail entirely. The problem is that their consequences ripple outward in ways most businesses, compliance teams, and even regulators are not equipped to track. Goods reroute through third countries. New intermediaries emerge overnight. Shell entities multiply. And global supply chains, already strained by post-pandemic reordering, absorb these detours with little transparency.

For trade professionals, this is not merely a policy concern. It is an operational reality with real legal, financial, and reputational stakes.

The Russia-Ukraine conflict provides the most vivid example of sanctions-driven trade route rewiring. Shortly after Russia's full-scale invasion in February 2022, maritime trade flows in the Black Sea were significantly reshaped.

Russia swiftly circumvented restrictions by employing a shadow fleet of older vessels with unclear ownership. In January 2025, 86% of Russia's crude oil exports were transported by the shadow fleet, with 94% of these vessels over 15 years old. Despite the US, UK, and EU sanctioning 311 oil tankers by February 2025, 63 sanctioned vessels continued lifting oil. The growth of the shadow fleet demonstrates how quickly alternative logistics networks can emerge when traditional shipping channels become restricted.

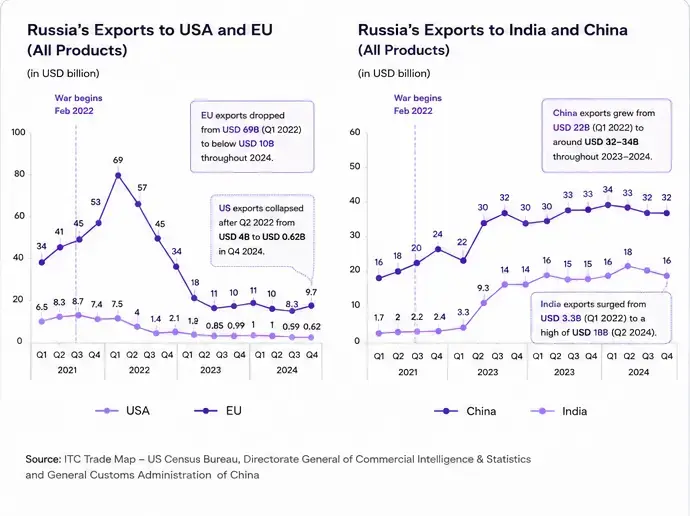

In 2024, Russia exported approximately USD 129 billion in goods to China, predominantly crude oil, coal, and natural gas, often at significantly reduced prices. China exported nearly USD 116 billion worth of goods to Russia in 2024, supplying machinery, electronics, and vehicles that replaced Western suppliers. China provided around 90% of Russia's technology imports in 2025, up from 80% in 2024.

The sharp decline in Russia's exports to the United States and the European Union after 2022 was accompanied by a significant increase in exports to China and India. While sanctions reduced Russia's access to Western markets, they also accelerated the redirection of trade toward alternative partners.

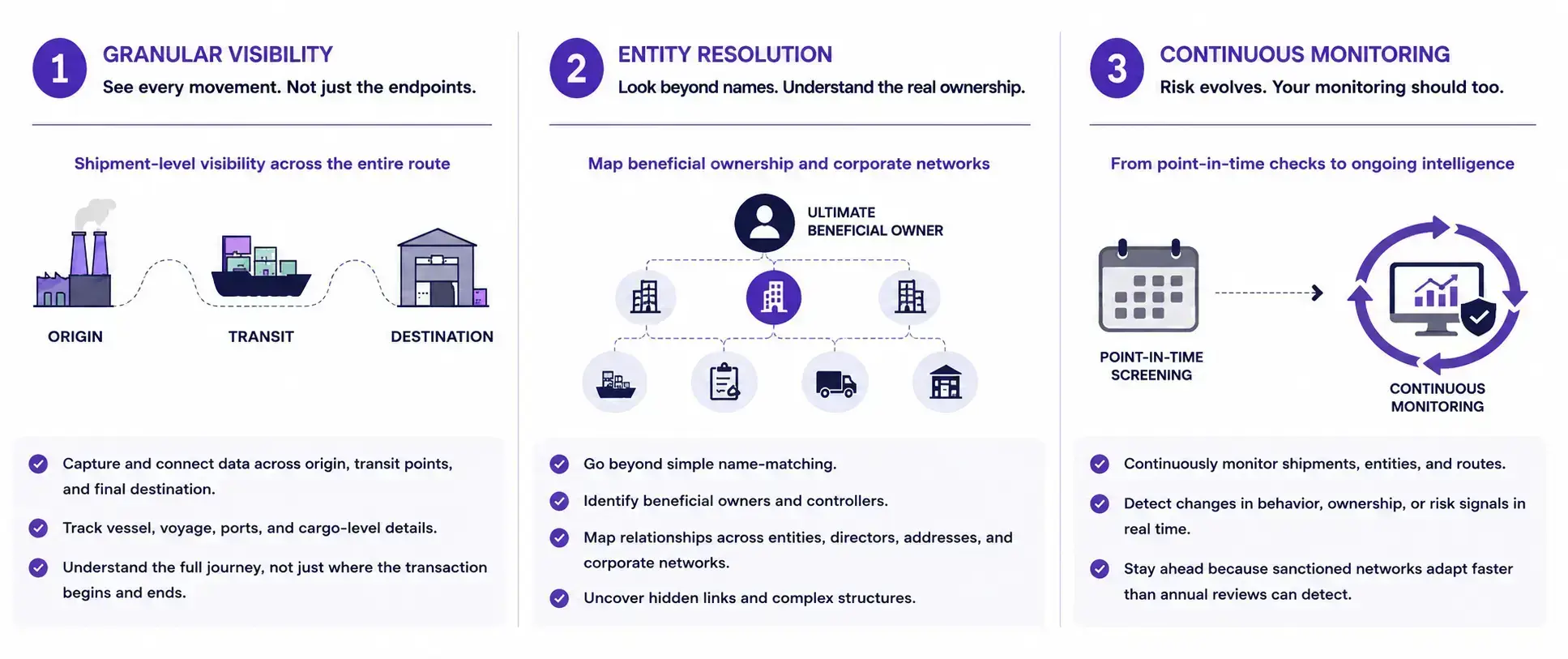

This shift underscores a growing challenge for businesses and regulators alike: sanctions are not simply restricting trade flows; they are rewiring them. As goods move through new corridors and commercial networks, identifying sanctions exposure requires greater visibility into counterparties, ownership structures, and trade routes than ever before.

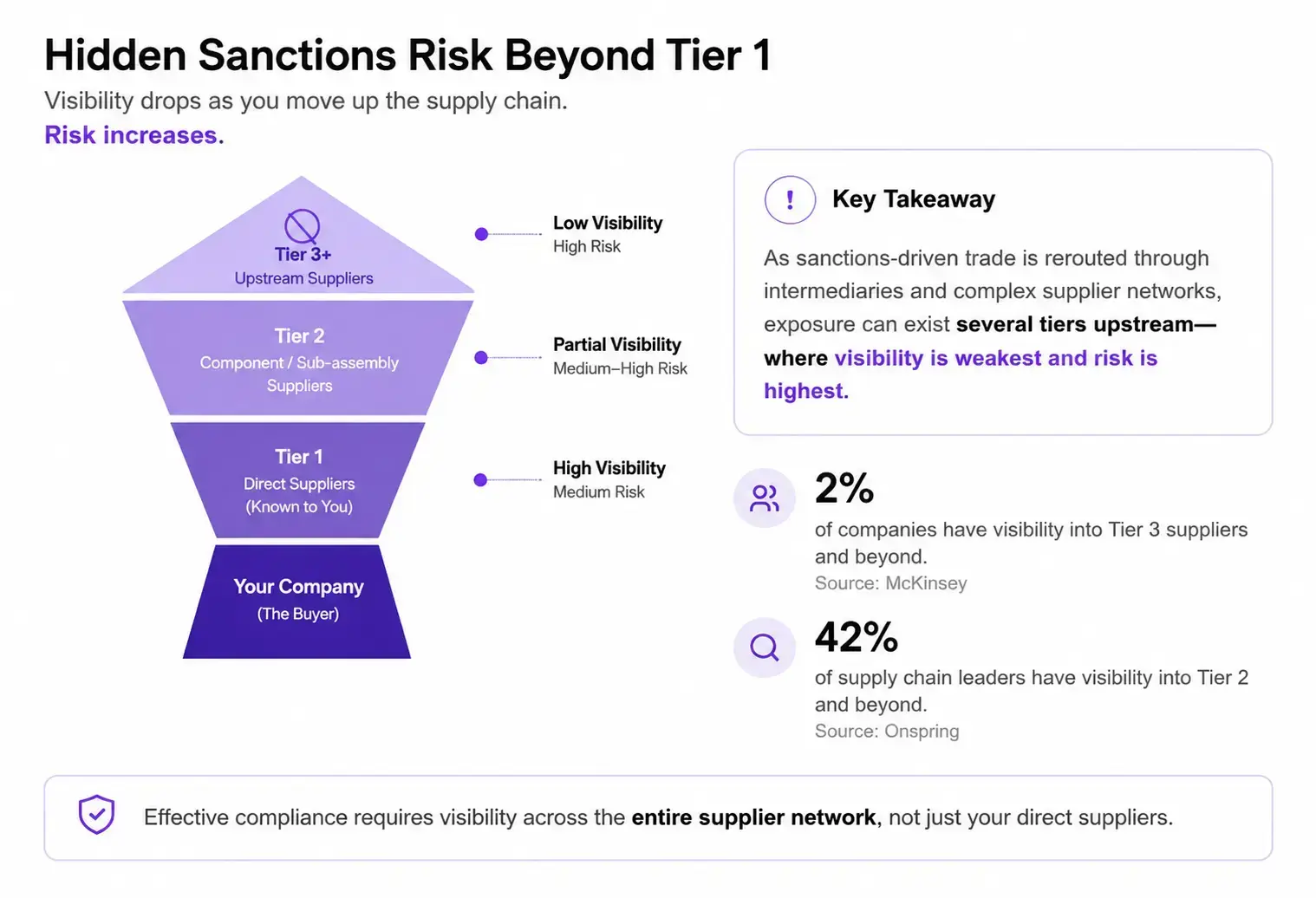

The impact of sanctions-driven trade rerouting extends beyond shipping lanes and trade corridors. It is increasingly reshaping supplier networks in ways that many businesses cannot easily see. As companies seek alternative sourcing channels through intermediary countries and new trading partners, sanctioned exposure can move deeper into the supply chain, beyond direct counterparties and into Tier 2 and Tier 3 supplier networks.

This creates a significant visibility challenge. A recent survey by McKinsey found that 95% of supply chain leaders report visibility into Tier 1 risks, but only 42% have visibility into Tier 2 suppliers and only 2% have visibility into suppliers in the third tier and beyond. At the same time, research suggests a meaningful share of supply chain disruptions originate in these upstream tiers, where oversight is weakest.

As trade flows become more fragmented and reliant on intermediaries, businesses may unknowingly source materials, components, or services that have passed through high-risk entities further upstream. In this environment, sanctions compliance is no longer just about knowing who you buy from. It increasingly requires understanding who your suppliers buy from as well.

Sanctions are meant to add pressure, not build perfect barriers. In practice, trade often finds a way around them. What we are seeing is trade becoming more flexible and harder to track. Shipping data is often incomplete, company ownership can be hidden, and goods can pass through transit hubs where enforcement is weak.

The countries that help redirect trade are not always acting in bad faith. Many are trade-dependent themselves and face their own political pressures. But hidden structures in these places can be used by people who are trying to evade sanctions.

For compliance teams, the job is now bigger than just checking names on a sanctions list. They need to look at the full network behind a deal: who owns the ship, who uses the freight forwarder, where the company is registered, and whether the product and destination match.

Regulators are starting to respond, but slowly. One growing tool is secondary sanctions, which can punish companies in third countries that help sanctions evasion. This means businesses in places like Singapore, India, or the UAE may face risk even if they are not directly dealing with a sanctioned party.

The rewiring of trade routes is not a temporary disruption. It is a structural shift in how global commerce moves under geopolitical constraint. Businesses that treat sanctions compliance as a static checklist will remain perpetually behind the curve. Those that build dynamic, intelligence-led approaches to trade monitoring will be the ones who navigate this landscape with confidence. In a world where trade routes can shift faster than regulations are updated, visibility is becoming as important as compliance itself.