Podcasts

Watch videos featuring supply chain experts

Imagine the operational reality a purchasing manager in Rotterdam faces on February 20, 2026. They’re about to issue a routine purchase order for about forty containers of components coming in from Southeast Asia, with the idea of having them folded into production in roughly nine weeks. Naturally the manager leans on the automated ERP stack and Global Trade Management (GTM) systems, because that’s what’s there, what’s reliable and quick. But those platforms basically run on an old, almost silent premise: that the maritime trade corridors stay stable, calm and pretty much predictable as constants, year after year. The workflow is legally fine, procedurally correct, all neat on paper. Still, even if everything looks compliant, the transaction stays extremely exposed to geopolitical turbulence, like a small crack that you can’t really see until it spreads.

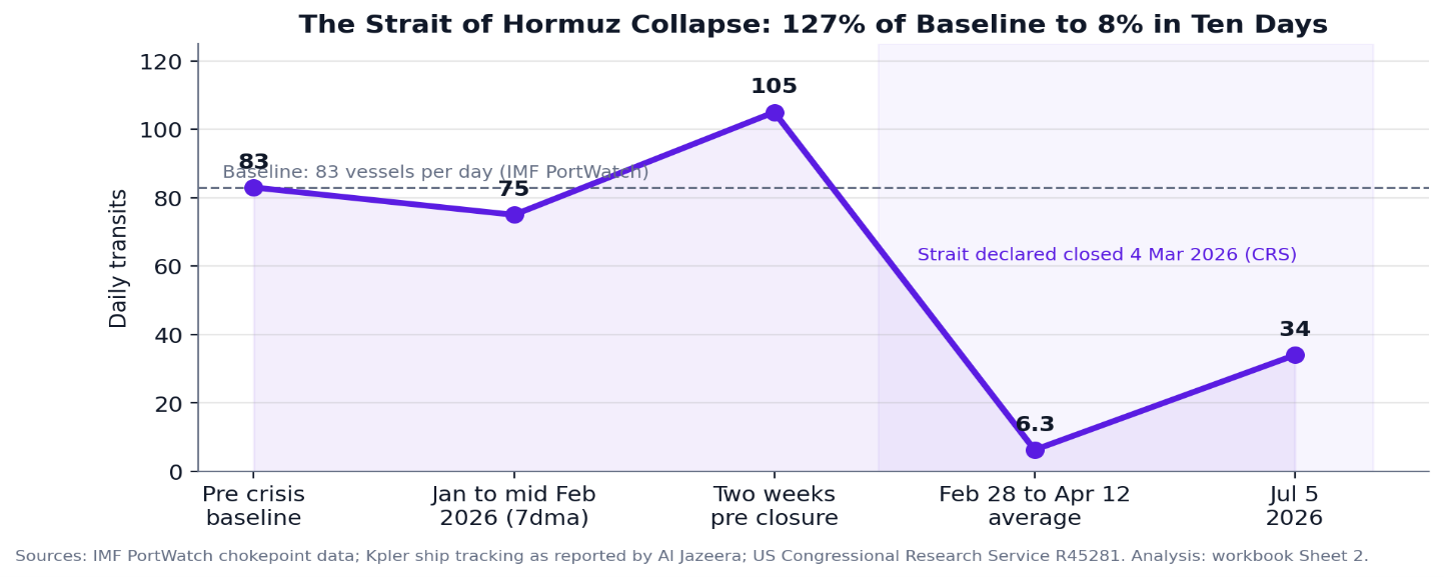

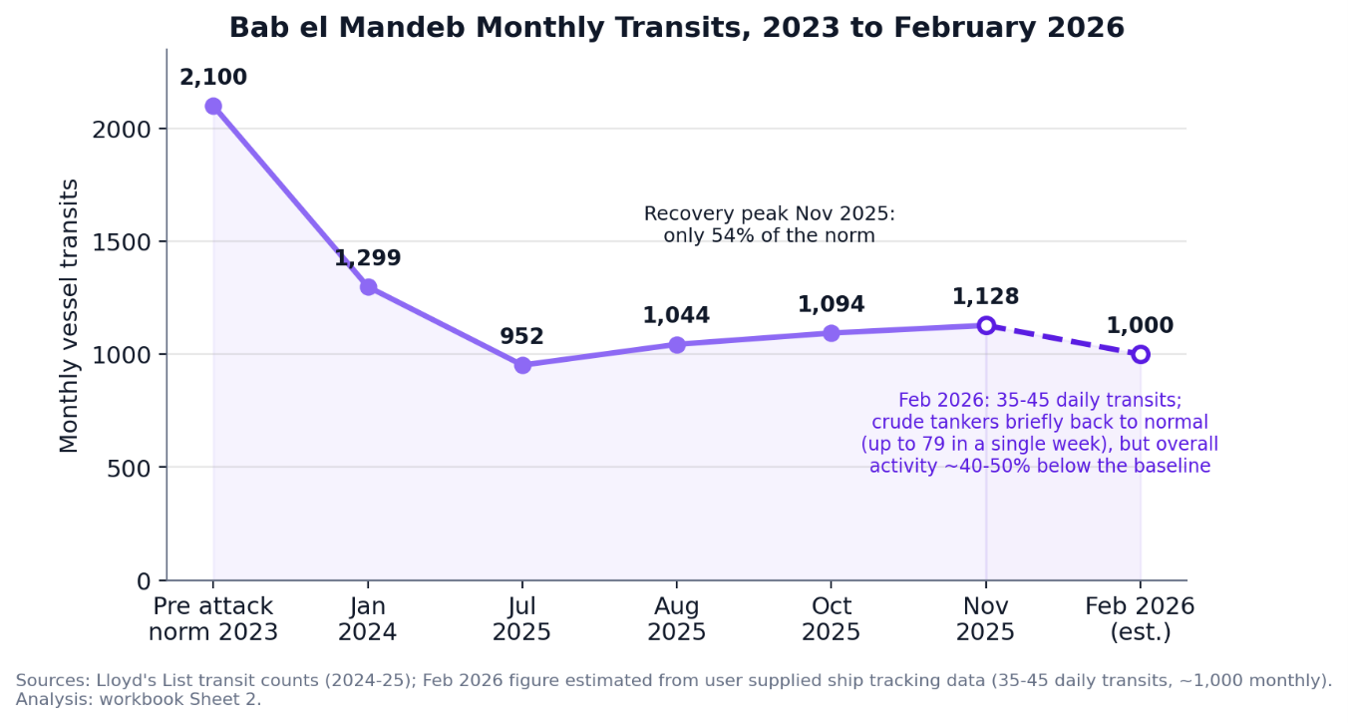

This reliance on stability is, well, pretty understandable. After a two-year disruption in the Red Sea, the main metrics up through late 2025 seemed to show a kind of surface restart, with passage through the Bab el-Mandeb strait hitting a two-year peak that November. Still, if you look more granularly, that baseline was a bit misleading, like, too clean. Even when the recovery looked strongest, traffic volumes only got to about two-thirds of what used to be normal, Suez Canal utilization sat under 50%, and fiscal revenues held onto a cumulative 33% gap across two cycles. In other words, the global shipping ecosystem hadn’t truly rebounded, it had just landed in a steadier but structurally weakened equilibrium. So when regional tensions spiked and made the Strait of Hormuz effectively shut down eight days later, the commercial assumptions of the order kind of unravelled. The strait, which usually supports roughly one-fifth of global oil and gas movement, saw daily vessel traffic crash from 127% of baseline down to under 10% in just ten days. That shock then flipped the fragile Red Sea “comeback” in sync, with tankers getting anchored, crews getting stranded, and oil prices spiking by nearly 50%. By the end, freight rates , transit schedules and even the customs assumptions behind the Rotterdam order were made irrelevant by geopolitical shifts that legacy automated systems couldn’t realistically anticipate.

This is the part of the story that matters most: nothing in their software failed. It did exactly what it was designed to do, which was to record the transaction faithfully after the fact. The failure was architectural. Tools were built for a world where geography holds still, and geography has stopped holding still.

A note before the numbers: the figures in the rest of this story come from a single analysis spreadsheet built alongside this report, which blends open chokepoint and insurance data with a simulated landed cost model resting on stated assumptions about freight rates, cargo values and carrying costs. Treat every number as an illustration of magnitude, not a quotation of anyone's invoice.

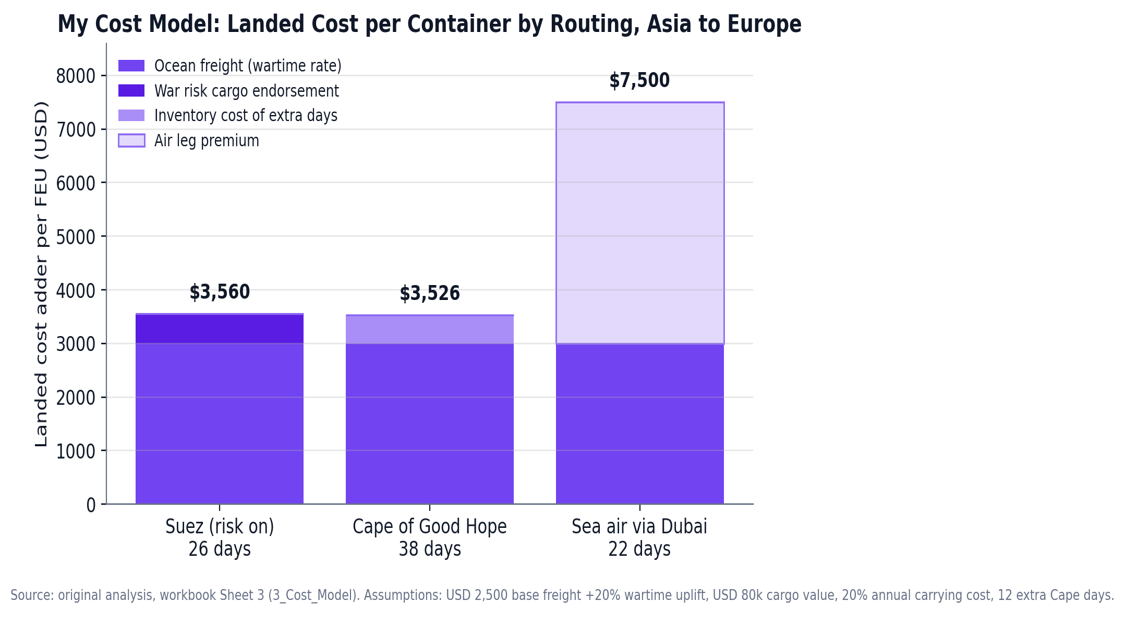

To fully quantify this vulnerability, one kind a have to dig into the obscured financial metrics of the disruption those variables that standard procurement software just sort of smooths over, like they’re not relevant. Even if cargo transit is still physically feasible through some alternative routing, the main financial impact quietly flips from direct freight rates to the cost of time. When the forty containers are redirected around the Cape of Good Hope the delta in base ocean freight tariffs is basically negligible, so the legacy ERP systems don’t really flag the detour, it’s like they simply don’t see it.

The real liability shows up later, in the extended transit times. If you add twelve extra days at sea for a container carrying $80,000 worth of inventory, you end up with roughly $526 per container in hidden costs. Those costs come from capital being tied up longer, the need to adjust safety stock, and also product shelf-life taking a hit, little by little. Spread that across the whole forty-container consignment, and then compounded again across all quarterly orders, that “low-cost” detour stops being low-cost at all. It becomes one of the organization’s biggest unbudgeted operational expenses, sometimes faster than anyone expects.

There’s another logistical framework too, one that legacy systems also fail to properly evaluate: an intermodal hybrid model. Think ocean freight first to a regional hub, then air freight for the components that are time sensitive. This route adds a premium of about $4,500 per container, but its whole reason for existing is time recovery. The approach recovers sixteen days of transit time at an implied $248 per day saved. Whether that hybrid model actually depends entirely on the time-value of the specific cargo. This is a computable, measurable metric just not in the standard corporate workflows. In practice it stays uncalculated at the single most critical inflection point, before purchase order authorization, where it would matter most.

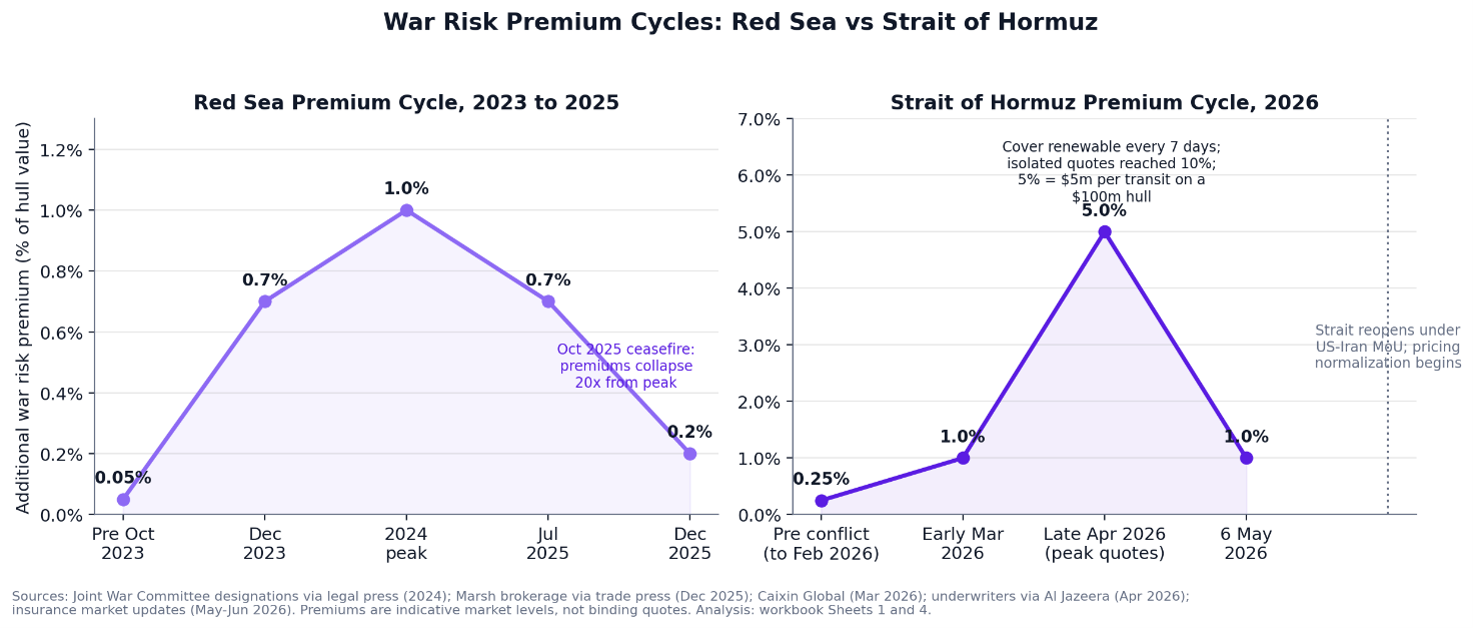

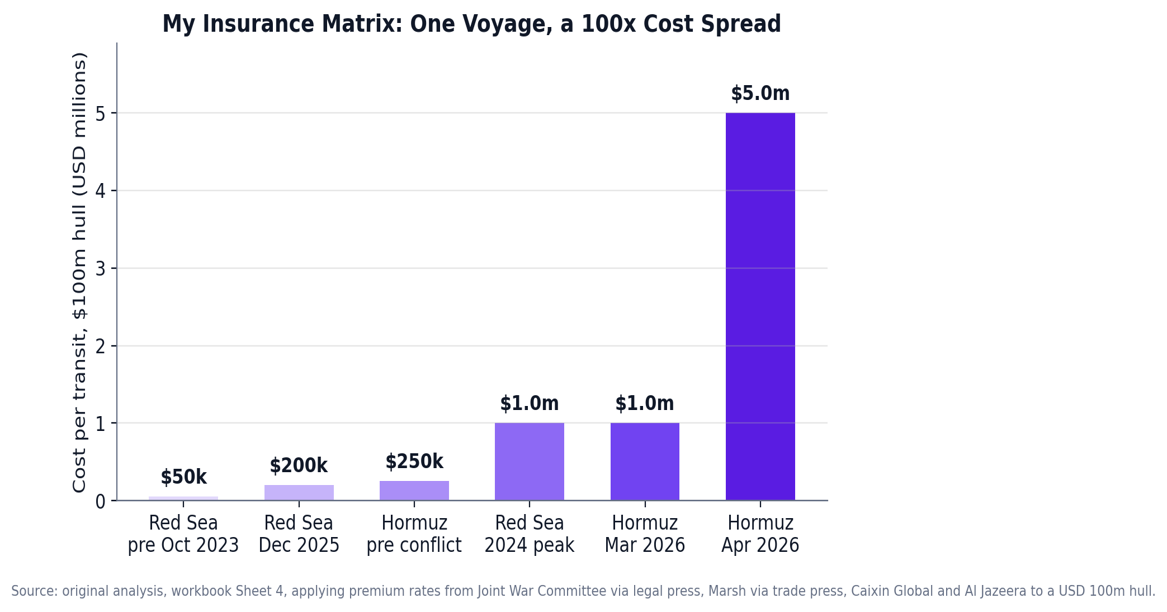

There is one more character in this story, and it moves faster than the ships: the price of courage. War risk insurance was once a rounding error, a sliver of a percent of a vessel's value, renewed and forgotten. Across the Red Sea years it learned to move like weather: a twenty fold climb as the attacks began, a long stormy plateau, then a sudden clearing after the late 2025 ceasefire brought it most of the way back down. Anyone who concluded the weather had broken for good was reading a cycle as an ending.

At the worst quotes of the spring, insuring one transit of a 100 million dollar hull cost about 5 million dollars, roughly a hundred times what the calmest corridor charged for the same content. Our spreadsheet's simulation makes the strategic point brutally simple: a vessel working that corridor continuously at the early crisis rate would accumulate an insurance burden in the tens of millions per year. When one input to landed cost can move a hundredfold inside eight weeks, insurance is no longer a surcharge to be passed through. It is a routing variable, as decisive as distance, and any cost engine that treats it as a constant is quietly wrong about every order it prices.

Next-generation Global Trade Management (GTM) software must evolve from a reactive, downstream record-keeping system into an autonomous, upstream operational layer integrated directly into the procurement phase before capital commitments occur. Operating ahead of the ERP ecosystem, a future-ready platform runs real-time transit simulations immediately upon order drafting. It dynamically prices geopolitical risk and war risk endorsements based on live conditions, calculates precise dollar-per-container-per-day carrying costs across all viable routes, and performs automated compliance and sanctions screening within seconds. Rather than causing alert fatigue when a shipping corridor exhibits elevated risk, the system autonomously proposes pre-priced, optimized multimodal alternatives (like sea-air or rail) and instantly switches fulfilment to the configuration offering the lowest total cost. Achieving this level of resilience requires a fundamental architectural shift: replacing batch processing with live data streaming, trading static rate cards for dynamic journey simulations, and utilizing automated delegated authority to compress approval chains. Ultimately, the value of a next-generation GTM system is judged not by its user interface, but by its ability to autonomously keep corporate operating margins intact when global supply chains disrupt.